Japan’s Stablecoin Rules

JPYC Co. launched what regulators and the company call the world’s first fully regulated yen-pegged stablecoin in October 2025, capping a decade of cautious financial architecture that Tokyo began laying well before most governments acknowledged digital money existed.

The milestone did not arrive by accident. Japan’s Financial Services Agency (FSA) spent years designing a framework that would make a collapse like Terra/Luna structurally impossible on its soil, and the rules it finalized through amendments to the Payment Services Act tell you exactly where the country’s priorities landed.

Japan Draws a Hard Line on Who Can Issue

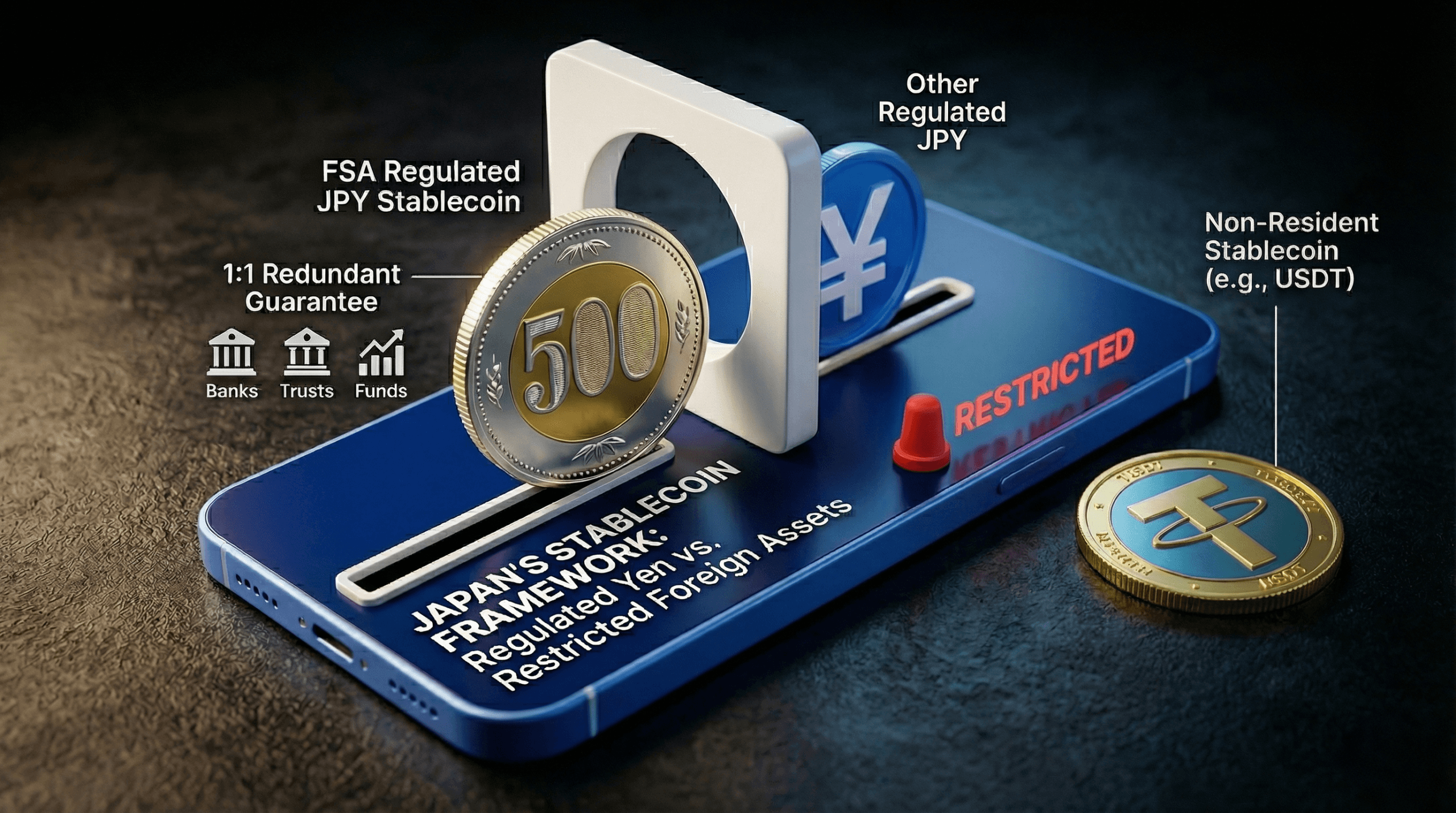

The PSA amendments, effective June 2023 with further refinements set to take effect by June 2026, draw a hard line around who can issue what the FSA calls “digital-money type stablecoins.” Only three types of licensed domestic entities qualify: banks, fund transfer service providers, and trust companies. Each issuer type carries its own reserve structure. Banks issue stablecoins as deposits covered by Japan’s existing deposit insurance system. Fund transfer service providers back their tokens with money deposits, bank guarantees or entrusted safe assets, including Japanese government bonds. Trust companies hold all trusted assets as bank deposits, with a post-2025 provision allowing up to 50% in low-risk short-term instruments.

JPYC became the first company to secure a fund transfer service provider license under the new regime in August 2025. Its yen-pegged token runs on Avalanche, Ethereum, and Polygon, carries a 1:1 yen reserve backing, and charges no transaction fees. Revenue comes from JGB interest earned on the reserve pool. The company has set a target of 10 trillion yen in circulation over three years, with a longer-term goal of 60 trillion yen within five years, focused on remittances, payments, and cross-border Web3 settlements.

The FSA designed this framework with one specific memory in mind. The 2022 Terra/Luna collapse, which wiped out tens of billions in value globally, hardened Japan’s existing caution into explicit law. Regulators concluded that the core risk in stablecoins is a run, the same dynamic that destabilizes conventional banks, and they built redemption at par as the system’s foundation. Every issuer is legally required to honor that guarantee. Tokens that cannot meet the standard are reclassified as crypto-assets and face an entirely different regulatory track.

Dollar Stablecoins Run Into a Wall

That architecture has a direct consequence for USDT and USDC. Dollar-denominated stablecoins control roughly 97 to 99% of the global stablecoin market, but they hold a fraction of that share in Japan. Foreign issuers like Tether and Circle cannot distribute to Japanese residents without meeting the same user protection and AML standards required of domestic entities, a bar that has rarely been cleared.

Japanese exchanges have historically avoided listing USD stablecoins rather than navigate the compliance structure. USDT remains largely restricted on Japanese platforms as of early 2026. USDC has a limited, regulated pathway via SBI VC Trade following Circle’s partnership with SBI Holdings, but access is capped and not broadly available to retail users.

The preference for yen-denominated digital assets is not entirely regulatory. Japan’s cash-heavy domestic economy generates less natural demand for dollar liquidity tools, and yen usage in regional remittances and trade already provides a functional alternative for cross-border needs. The FSA framework reinforced existing market behavior rather than working against it.

Banks Are Moving In

Japan’s three largest banks, MUFG, SMBC, and Mizuho, are developing trust-based yen stablecoins through the Progmat platform via joint proof-of-concept programs. SBI Holdings has announced plans to launch a yen stablecoin in Q2 2026. The total JPY stablecoin market cap sits at approximately $36.6 million as of early 2026, modest against global USD volumes but growing in the institutional and cross-border payment segments where Japan’s framework actually functions well.

Middlemen Face Their Own Stack

Intermediaries operating in this space face their own compliance requirements. Buying, selling, custodying, or transferring digital-money type stablecoins requires registration as an Electronic Payment Instrument Exchange Service Provider. Registered firms must hold at least 95% of customer crypto-assets in cold storage, segregate user funds in trust structures, comply with FATF Travel Rule requirements, and enter into contractual liability-sharing agreements with issuers covering losses from bankruptcy, hacks, or technical failures.

The 2025 PSA Amendment Act, enacted in June 2025, adds a lighter intermediary category for pure brokers, relaxes some reserve rules for trust-type issuers, and creates more flexibility for cross-border handling. FSA consultations from January 2026 addressed which bond types qualify as eligible reserves. The agency is also reviewing whether certain crypto-assets should move from PSA oversight to the Financial Instruments and Exchange Act, a change that would not affect the stablecoin framework but could alter investor protections for other digital assets.

How Japan Got Here

Japan’s early regulatory history helped set the conditions for where the market landed today. The 2014 Mt Gox collapse, then the world’s largest exchange, pushed the government into the first PSA crypto amendments by 2016. Those rules required exchange registration, user asset segregation and AML compliance for crypto broadly. Stablecoins received little attention in that early framework because the products barely existed. JPYC’s predecessor product, launched in 2021 as a Prepaid Payment Instrument rather than a formal stablecoin, and Hokkoku Bank’s regional Tochika token in Ishikawa Prefecture were the most visible early experiments before the current regime took shape.

The system Japan built is deliberate about what it sacrifices. It moves slowly. It favors domestic issuers. It keeps the largest global stablecoins effectively sidelined. What it produces in exchange is a structure where every yen-pegged token in circulation carries a redemption guarantee, a licensed issuer, a segregated reserve, and FSA oversight. That tradeoff will look different depending on whether you are a Tokyo retail user, a megabank treasury desk, or a foreign exchange trying to list USDC.

What Comes Next

More bank launches are expected in 2026. JPYC is expanding interoperability through a partnership with Circle and a TIS integration for enterprise payments. The framework that limited stablecoin activity for years in Japan is now the same framework enabling the first regulated domestic issuances. Whether that pace satisfies the market is a separate question from whether the system works as designed.

FAQ 🔎

- What stablecoins are legal in Japan? Only yen-pegged digital-money type stablecoins issued by FSA-licensed banks, fund transfer service providers or trust companies are legal for circulation to Japanese residents.

- Is USDC or USDT available in Japan? USDT remains largely restricted on Japanese platforms, while USDC has limited regulated access via SBI VC Trade under a Circle partnership.

- What is JPYC? JPYC is the first fully regulated yen-pegged stablecoin, launched in October 2025 by JPYC Co. under Japan’s revised Payment Services Act framework.

- Why does Japan restrict foreign stablecoins? Japan’s FSA requires all stablecoin issuers targeting residents to meet the same user protection, reserve, and AML standards as domestic licensed entities, a threshold most foreign issuers have not cleared.