Digital assets are forms of value stored and exchanged in digital formats, including crypto assets, stablecoins, NFTs, tokenized real-world assets, and central bank digital currencies. Unlike traditional money, they exist only electronically, secured by blockchain technology and cryptography, allowing ownership, transfer, and transactions without intermediaries.

In this article, we will break down the key characteristics of digital assets, explore the different types available, and explain how investors and businesses can generate income, manage risks, and stay compliant with IRS rules. You will also discover practical steps to get started, along with clear guidance on storage, security, and strategic participation in the digital economy.

What Are Digital Assets?

A digital asset is any asset that exists in a digital form, is stored electronically, and holds measurable value or ownership. At a functional level, digital assets serve as representations of value, rights, or data. Within the financial industry, many serve as investment products, a medium for payments, or tools for cross-border payments. Outside finance, digital assets also provide access to services, content, and other resources.

Some digital assets operate on blockchain technology, which uses a distributed ledger where transactions are recorded across multiple nodes. This removes dependence on financial institutions and enables direct verification of ownership. Such systems also support decentralized finance, where users interact without intermediaries.

In contrast, a central bank digital currency is issued and managed by a central bank, designed to function like physical currency in a digital environment. This form of digital money remains under government control, unlike decentralized alternatives.

The scope of digital assets extends beyond finance into broader use cases. Other digital assets include files in various formats, licensed content tied to intellectual property, and tokenized real-world assets. Each carries defined ownership and can be transferred or monetized.

Key Characteristics of Digital Assets

- Decentralization: Decentralization removes reliance on a central authority, such as banks or a central bank. Many crypto assets and virtual currencies operate on a distributed ledger, where control is spread across a network of nodes. This structure reduces single points of failure and allows direct transactions between users without intermediaries.

- Security: Security relies on cryptography and system design. Access to assets is controlled by a private key that verifies ownership and authorizes transfers. Strong encryption protects data from unauthorized access, while weak key management exposes assets to loss or theft. Secure systems focus on how assets are stored, accessed, and transferred.

- Transparency: Transparency comes from public recordkeeping. On blockchain networks, every transaction is recorded and visible, allowing users to verify activity in real time. This level of openness reduces manipulation and builds trust without relying on financial institutions.

- Immutability: Once data is recorded, it cannot be altered. A confirmed transaction on a blockchain becomes part of a permanent history. This protects the integrity of ownership records and prevents unauthorized changes to asset data.

- Programmability: Enables digital assets to operate via smart contracts. These are self-executing codes that trigger actions when conditions are met. This capability powers financial applications, automated payments, and systems within decentralized finance.

- Liquidity: The ease with which an asset can be converted into cash or exchanged. Many digital assets are actively traded on exchanges, allowing quick entry and exit. High liquidity creates more investment opportunities, while low liquidity can limit the ability to sell without affecting the price.

Types of Digital Assets

Digital assets cover a wide range of use cases across finance, technology, and business. Each type serves a different purpose, from enabling payments to representing ownership of real-world assets.

1. Cryptocurrencies

Cryptocurrencies are digital assets that operate as a form of digital currency. They rely on blockchain technology and a distributed ledger, which records every transaction across a network of computers. This system removes reliance on a central bank while maintaining verifiable ownership. Because these assets can serve as a medium of exchange, a store of value, and a unit of account, active markets allow investors to trade them, opening new investment opportunities.

2. Stablecoins

Stablecoins maintain a consistent value by being pegged to physical currency or backed by reserves. Their stability makes them useful for fast, predictable payments and cross-border transactions. Platforms and financial institutions increasingly adopt stablecoins to reduce volatility and enable smooth transitions between traditional finance and crypto assets.

3. Non-Fungible Tokens (NFTs)

Non-fungible tokens represent unique digital items whose ownership is permanently recorded on a blockchain. Unlike cryptocurrencies, each NFT carries distinct attributes, making substitution or duplication impossible. This uniqueness allows NFTs to function as digital art, collectibles, or intellectual property. Verification on the blockchain ensures authenticity and traceable ownership, giving creators and holders confidence in asset integrity.

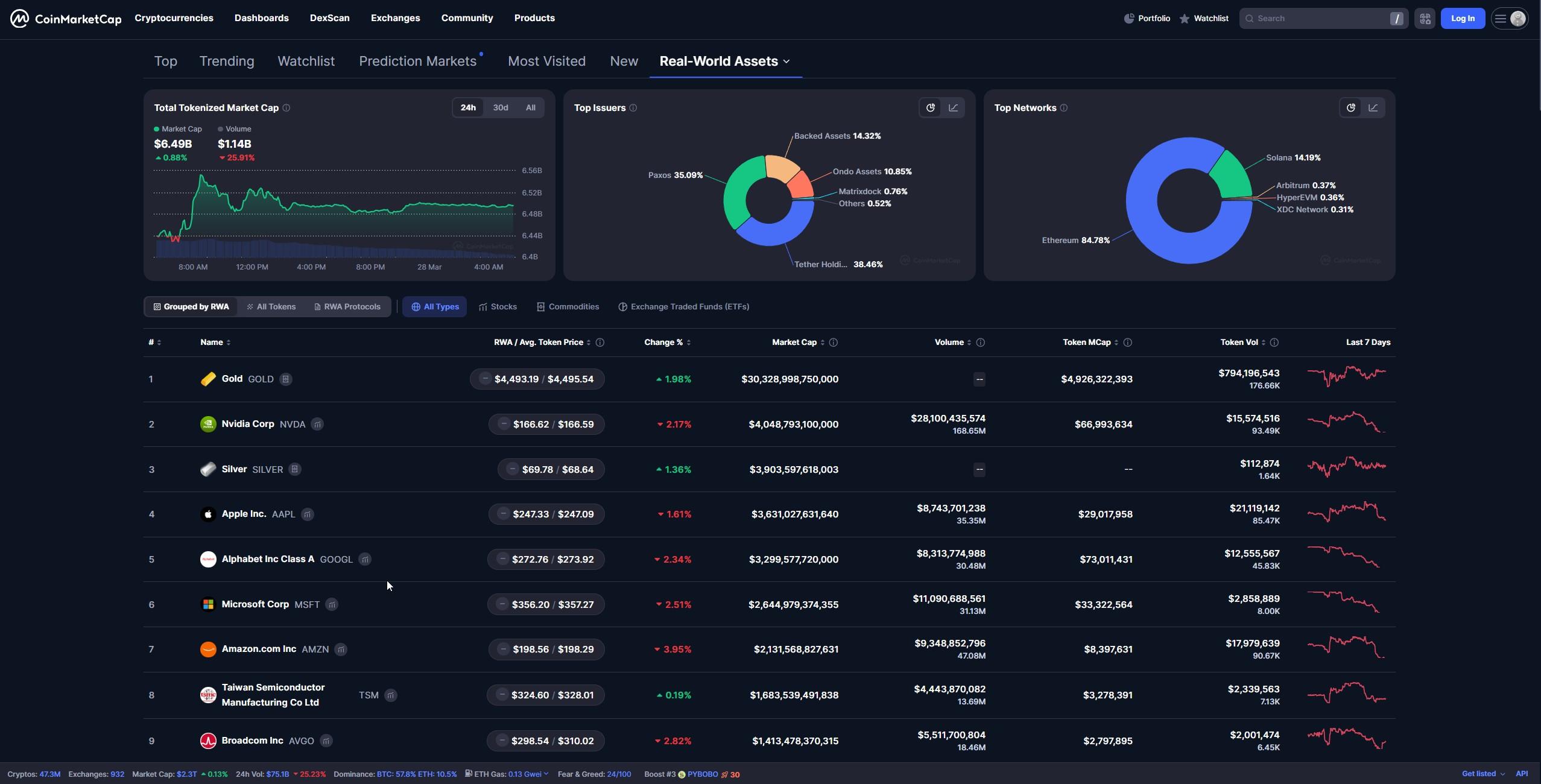

4. Real-World Asset Tokens (RWAs)

Real-world asset tokens convert physical assets, such as real estate, commodities, or equities, into digital tokens. Tokenization enables these assets to be divided, transferred, and traded efficiently, increasing accessibility for investors who previously lacked access to traditional markets dominated by financial institutions. This process also improves liquidity and transparency across digital marketplaces.

5. Central Bank Digital Currencies (CBDCs)

Central bank digital currencies are issued and regulated by a central bank and serve as digital equivalents of fiat money. They combine the efficiency of digital payments with government oversight, providing secure, standardized transaction options while maintaining control over monetary policy.

6. Intellectual Property Rights

Digital assets also include ownership of intellectual property in formats such as software, music, videos, or written content. Managing these assets requires a digital asset management system, which allows companies or creators to organize, securely store, and track access. Proper data management ensures that ownership remains verifiable and content remains accessible over time.

Why Do Digital Assets Matter?

Digital assets have transformed how value is created, transferred, and stored in both personal finance and the broader economy. Their relevance stems from the unique combination of accessibility, transparency, and programmability, which traditional assets cannot match. Below are the main ways digital assets impact individual investors and businesses worldwide.

For Individual Investors

For individual investors, digital assets provide direct control over ownership and transactions. Access is provided through secure wallets, eliminating reliance on banks or intermediaries. The ability to trade, stake, or monetize assets opens multiple investment opportunities, while blockchain technology ensures verifiable ownership and transaction history.

This transparency reduces counterparty risk and enables investors to participate in markets previously limited by geography or capital requirements. Digital assets also offer diversification across crypto assets, stablecoins, NFTs, and tokenized real-world assets, helping investors balance risk and capture potential gains in the digital economy.

For Businesses and the Global Economy

For businesses, digital assets streamline operations, reduce transaction costs, and expand market reach. Companies can tokenize products, manage intellectual property, and leverage digital asset management systems to organize and securely store valuable data. On a global scale, digital assets enhance cross-border payments, enable faster settlement, and improve transparency in financial applications.

Governments and central banks are exploring central bank digital currencies to modernize financial infrastructure, increase efficiency, and maintain oversight of economic activity. The adoption of digital assets fuels innovation, creates new services, and drives the expansion of the global digital economy.

How Do Digital Assets Make Money?

Digital assets offer multiple avenues for generating value, combining traditional investment strategies with unique opportunities exclusive to the digital economy. Each method builds on ownership, transferability, and programmability, allowing both individuals and businesses to capture returns.

1. Investing and Trading

Investing and trading involve buying digital assets at one price and selling at a higher price to capture gains. Active markets for crypto assets, stablecoins, and tokenized real-world assets create opportunities for short-term trading or long-term holding. Transparent blockchain records ensure verifiable ownership and reduce counterparty risk, while access to exchanges allows participation across global markets without geographic limitations.

2. Staking and Yield Farming

Locking digital assets into networks or liquidity pools through staking and yield farming can generate attractive returns. Staking helps secure blockchain networks while earning rewards, whereas yield farming involves providing liquidity for decentralized finance platforms. Both methods turn idle assets into investment products, creating predictable streams of digital income while supporting network operations.

3. Creating and selling NFTs

Non-fungible tokens allow creators to convert digital art, collectibles, or intellectual property into sellable digital assets. Ownership is recorded on blockchain technology, providing authenticity and traceable provenance. Selling non-fungible tokens offers direct monetization, and programmable smart contracts can enforce royalties for future sales, creating ongoing revenue from digital creations.

4. Monetizing Digital Content

Digital assets encompass content ownership in formats such as software, videos, and written material. A digital asset management system enables creators or companies to securely store, manage, and monetize content. Platforms and marketplaces allow access to broader audiences, turning intellectual property into revenue streams while maintaining verifiable ownership and control.

5. Lending

Digital asset lending provides income by temporarily transferring ownership to borrowers in exchange for interest or fees. Lending platforms operate with collateral and smart contracts to ensure repayment, combining financial applications with automation. This method generates passive income while increasing liquidity in decentralized finance markets.

What Are the Risks of Digital Assets?

Digital assets provide new ways to invest, transact, and store value, but these opportunities come with inherent risks. Understanding these risks helps protect ownership and navigate the market effectively. Below are the key areas of concern for anyone handling digital assets:

- Volatility: Prices for crypto assets, NFTs, and tokenized real-world assets can swing dramatically in short periods. High volatility can amplify gains but also increase the risk of rapid losses.

- Security Risks: Access relies on private keys, and their loss or theft can permanently deprive users of control over assets. Weak encryption, phishing, and insecure storage are major threats that require robust digital asset management.

- Regulatory Uncertainty: Evolving rules around central bank digital currencies, virtual currencies, and tokenized assets can affect market access, taxation, and legal protections. Policy shifts can have immediate financial consequences.

- Operational Risks: Platform failures, technical glitches, or smart contract vulnerabilities can disrupt transactions or result in permanent asset loss. Careful evaluation of platforms and contract mechanisms reduces exposure.

- Liquidity Risk: Some digital assets, particularly niche NFTs or tokenized assets, may have limited buyer demand. Low liquidity can delay conversions into cash or force sales at lower-than-expected prices.

What Does the IRS Consider a Digital Asset?

The IRS considers a digital asset as property, not currency. This means crypto assets, stablecoins, NFTs, and tokenized real-world assets are treated like stocks, bonds, or other investment products for tax purposes.

Any sale, exchange, or use of digital assets to buy goods or services triggers a taxable event. Receiving digital assets as payment, rewards, or through staking counts as taxable income, valued at the fair market price at the time of receipt. Proper record-keeping of all transactions is essential for reporting gains, losses, and income accurately.

In short, ownership, transfers, and use of digital assets have tax implications similar to those of property, making accurate tracking and compliance critical for investors and businesses alike.

How Can You Get Started with Digital Assets?

Starting with digital assets requires planning, secure storage, and an understanding of ownership and transactions. Proper steps reduce risk and help capture opportunities efficiently.

For Individuals

- Choose a secure digital wallet to store, manage, and access crypto assets or tokenized holdings.

- Select reputable exchanges for safe trading, investing, or participating in staking and yield farming.

- Understand different asset types, market behavior, and available investment opportunities before committing capital.

- Protect assets with strong security practices, including private key backups and two-factor authentication.

- Access educational resources to stay informed on market trends, regulatory changes, and technological developments.

For Businesses and Enterprises

- Implement a digital asset management system to organize, securely store, and track digital ownership.

- Tokenize products, intellectual property, or real-world assets to increase liquidity and create new revenue streams.

- Partner with regulated exchanges, payment processors, or financial institutions to ensure legal and tax compliance.

- Establish internal policies for data management, access control, and security to safeguard assets.

- Utilize digital assets to enhance operations, including faster cross-border payments, automated transactions, and new services.

Conclusion

Digital assets represent a transformative shift in how value, ownership, and transactions are handled in the modern economy. From crypto assets and stablecoins to NFTs and tokenized real-world assets, these instruments offer new investment opportunities, programmable functionality, and direct control over ownership.

Understanding the risks, tax implications, and proper management practices is essential for both individuals and businesses. Starting with secure storage, informed strategies, and reliable platforms ensures participation in the digital economy is safe, efficient, and poised for growth.

FAQs

Examples include crypto assets, stablecoins, NFTs, tokenized real-world assets, central bank digital currencies, and digital ownership of intellectual property.

Yes, digital assets are secure when stored with private key protection, encrypted wallets, and trusted digital asset management systems. Risks include hacking, phishing, and poorly maintained platforms.

Yes, digital assets provide investment opportunities and potential gains, but high volatility and market risk require careful research, strategy, and capital allocation.

Yes. The IRS treats digital assets as property, meaning gains, sales, exchanges, and income from staking or rewards must be reported for taxes.

Use hardware wallets, encrypted software wallets, and reliable digital asset management systems. Backups and secure private key storage are essential to prevent loss.

Access depends on proper planning. Private keys or wallet credentials should be securely passed to heirs or included in estate plans to ensure control and transfer of assets.